The Central Provident Fund (CPF) plays a crucial role in securing the financial future of Singaporeans by providing for retirement, healthcare, and housing needs. As of January 2025, several key changes to CPF contribution rates and salary ceilings have taken effect. These updates impact employees, employers, and retirees, with a focus on improving retirement adequacy.

Increased CPF Contribution Rates for Senior Workers

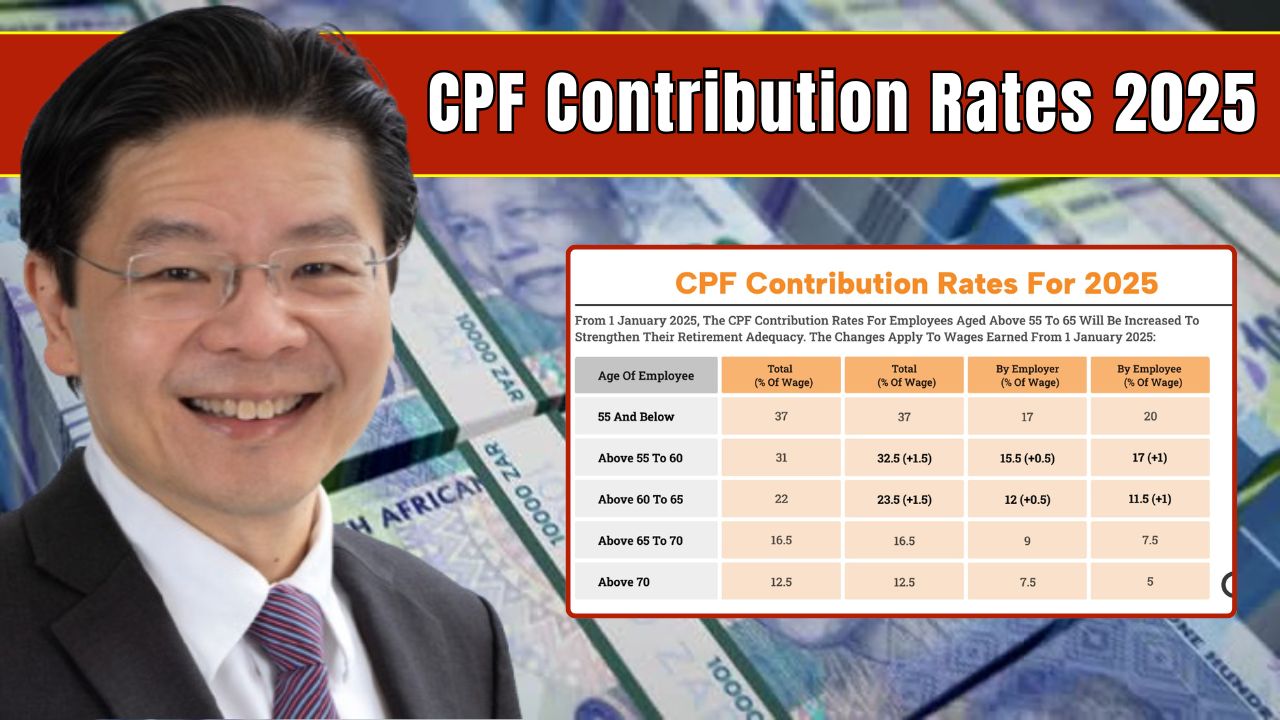

To strengthen retirement savings for older employees, CPF contribution rates for workers aged 55 to 65 have increased. The combined contribution rate has risen to 32.5%, up from 31% in 2024. Employees in this age group will contribute 17%, while employers will contribute 15.5%. This adjustment aligns with the government’s long-term plan to help older workers save more for retirement.

Adjustment of CPF Monthly Salary Ceiling

To ensure higher-income earners contribute a fairer share to their CPF, the monthly salary ceiling has been raised to $7,400, an increase from $6,800 in 2024. This change means individuals earning above this threshold will now have a greater portion of their salary subject to CPF contributions, leading to higher retirement savings.

Closure of Special Account (SA) for Members Aged 55 and Above

A major structural change in 2025 is the closure of the Special Account (SA) for members aged 55 and above. Savings from the SA will be transferred to the Retirement Account (RA), simplifying the CPF system and ensuring funds are allocated directly for retirement needs.

Increase in Enhanced Retirement Sum (ERS)

The Enhanced Retirement Sum (ERS) has been raised to $426,000 in 2025. This allows members to set aside more in their CPF Retirement Account, leading to larger monthly payouts in retirement. Those who choose to commit additional funds will benefit from more stable and secure long-term financial support.

Implications for Employees and Employers

For employees, these changes mean a higher portion of their salary will go into CPF, reducing take-home pay but strengthening long-term financial security. Older workers, in particular, will benefit from enhanced savings that support their retirement.

For employers, adjustments must be made to payroll systems to accommodate the increased CPF contribution rates and salary ceiling. The government has introduced a CPF Transition Offset, covering 50% of the increase in employer CPF contributions, helping businesses manage additional costs.

Conclusion

The CPF changes in 2025 reflect Singapore’s commitment to strengthening retirement adequacy while ensuring sustainable long-term financial planning for workers. Employees and employers alike should take note of these revisions to maximize benefits and ensure compliance with updated regulations.